The system of Central Provident Fund (CPF) in Singapore is changing in 2025 with the new rates of contributions and payment ceiling. The shifts are directed toward fortifying retirement savings particularly among the elder employees, and keeping up with the increment in wages and cost of living. As an employee, employer, or self-employed person, the CPF Contribution Table 2025 will be necessary in terms of financial planning and compliance.

Updated Contribution Rates by Age Group

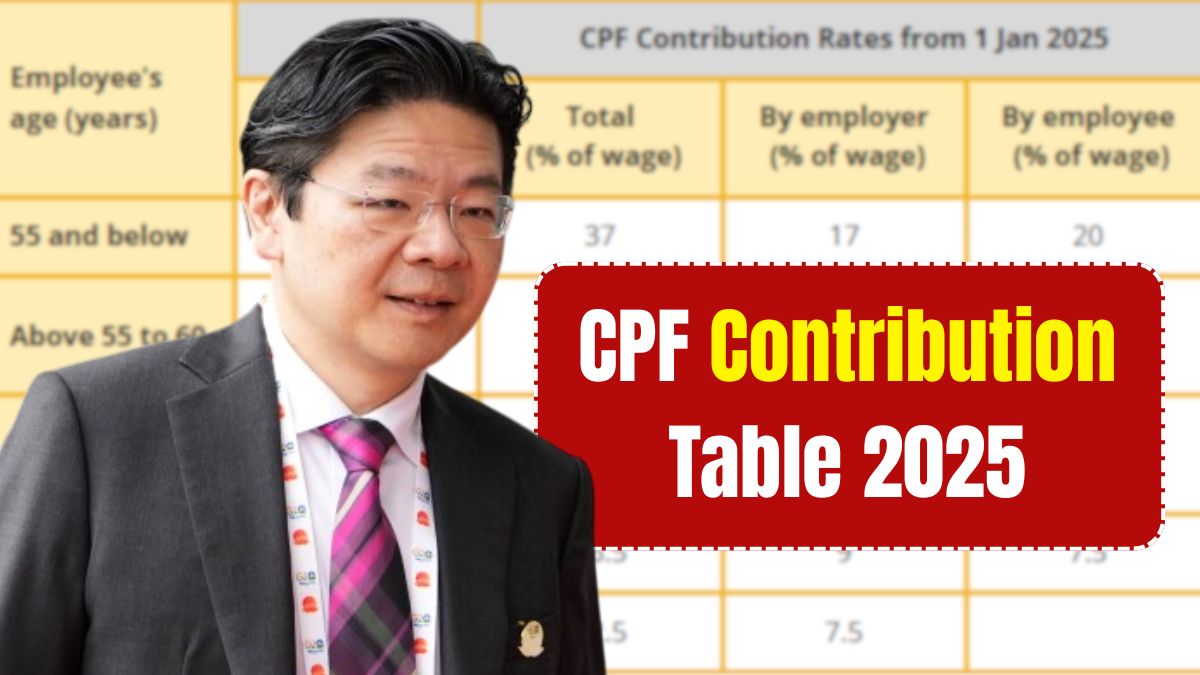

Even after 1 January 2025, the rate of CPF contribution will be at 37 (twenty by employees and seventeen by the employers) among those under the age of fifty five. Increasingly older people, the total rate is 32.5 percent in the range of 55 to 60 and the employees of 60 to 65 pay 23.5 percent. The contributions decrease more to persons above 65, signifying a tendency to retirement.

Revised Wage Ceilings

The Ordinary Wage (OW) ceiling is increasing to S$7,400 in monthly salary, which is an increment of S$6,800. What this implies is that CPF contributions will be levied today on even a higher percentage of monthly incomes. The Additional Wage (AW) limit of S$102, 000 a year has been maintained, less the OW to be subjected to OW drawback of the year.

Contribution Breakdown Example

A 60 years old worker who earns more than S$750 a month will contribute a total of 23.5% as CPF and this includes 12 percent contribution by the employer and 11.5 percent by the employee. The contributions are distributed between Ordinary Account (OA), Special Account (SA) and MediSave Account (MA), and serve to afford housing needs, retirement, and healthcare.

Support for Lower-Income Workers

Phasing out of CPF contribution is made on employees who earn between S$500 and S$750. This also means that lower-income earners will be able to save money without necessarily cutting down their after-tax pay checks. Employers continue to contribute partially, even though those who earn S$500 or back are not obliged to contribute.

CPF for Older and Self-Employed Workers

The CPF scheme also covers the needs of old laborers and self-employed by further extending its scope. Although the rate of contribution decreases as we age, voluntary top-up is encouraged by the government and matching grants under schemes such as the Matched Retirement Savings Scheme (MRSS). This means that individuals with low balances are able to increase their retirement savings.

Conclusion

It is CPF Contribution Table 2025 that is an indication of how Singapore is progressive in its retirement security. The system is geared to fulfill the changing requirements of diverse workforce, with more generous wage ceilings and spec aimed contribution changes. Being in the know when it comes to such changes is the best way to ensure that both the employers and employees are able to exploit the benefits of CPF as time goes by.

Also Read: CPF Housing Grant 2025 Explained: Eligibility, Amounts and Key Changes